5-year fixed*

5-year Varible*

Below are the current mortgage rates offered by Canada’s Big 6 banks as of February 11, 2025. Please note that these rates are subject to change and may vary based on individual circumstances.

| Bank | 5-Year Fixed | 5-Year Variable | 3-Year Fixed |

|---|---|---|---|

| RBC Royal Bank | 4.59% | 4.75% (Prime – 0.45%) | 4.64% |

| TD Bank | 4.74% | 4.84% (Prime – 0.36%) | 4.59% |

| Scotiabank | 4.69% | 4.50% (Prime – 0.70%) | 4.64% |

| BMO | 4.49% | 4.80% (Prime – 0.40%) | 4.30% |

| CIBC | 4.49% | 4.40% (Prime – 0.80%) | 4.79% |

| National Bank | 4.84% | 4.70% (Prime – 0.50%) | 4.89% |

| Bank | 5-Year Fixed | 5-Year Variable | 3-Year Fixed |

|---|---|---|---|

|

3.61% |

3.87% |

3.94% |

Fixed Rates: The interest rate remains constant for the term of the mortgage.

Variable Rates: The interest rate can fluctuate based on the bank’s prime rate. They are often expressed as “Prime +/- X%”. This is why most people complain when the Bank of Canada raises their rates.

Are you navigating the complex world of Canadian mortgages? Whether you’re a first-time homebuyer or considering refinancing, staying informed about the latest mortgage rate trends is crucial in Canada’s ever-changing real estate market.

Good news for homebuyers! The average 5-year insured fixed mortgage rate has decreased to 4.87%, dropping 8 basis points from last week and 5 basis points from last month. This trend could mean significant savings over the life of your loan.

For those looking at shorter terms, the 3-year fixed-rate insured mortgage is now at 5.32%, showing a 9 basis point decrease both weekly and monthly. This option might be attractive if you’re expecting rates to drop further in the near future.

The 5-year variable and adjustable mortgage rates have seen a slight uptick, rising 1 basis point to 4.87%. However, they’re still 21 basis points lower than a month ago, indicating an overall downward trend.

Meanwhile, 3-year variable and adjustable rates remain steady at 5.68%, unchanged from last week but down 25 basis points from last month. This stability might appeal to those comfortable with some rate fluctuation.

Remember, 1 basis point equals 0.01%. So, when you see a change of 8 basis points, that’s a 0.08% difference in your mortgage rate – which can add up to substantial savings over time!

These rate changes can significantly impact your mortgage payments and long-term financial planning. Whether you’re a first-time homebuyer or looking to refinance, it’s crucial to stay informed and consider all your options.

For personalized advice and competitive rates, consider reaching out to Canada Home Ownership.

Stay tuned for more updates from trusted sources like the Bank of Canada and Canada Mortgage and Housing Corporation (CMHC). Their insights can help you make informed decisions in Canada’s ever-changing housing market.

Remember, the right mortgage can save you thousands over the years. Don’t hesitate to explore your options and find the best fit for your homeownership dreams!

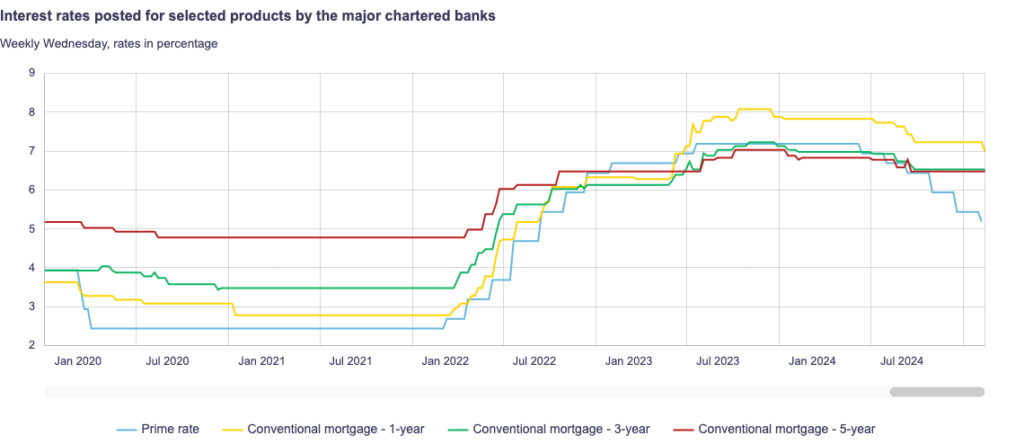

Source: bankofcanada.ca

Welcome to our Frequently-Asked Questions (FAQ) section, where we answer the most popular questions our Canada Home Ownership mortgage advisors receive daily, designed to help you make informed mortgage decisions whenever you need a new mortgage or renew/refinance an existing one.

Mortgage shopping can be confusing, especially if you're a first-time home buyer. There are a lot of different terms and options out there, and it can be tough to know where to start. This section will cover some of the most common questions and terms when shopping for a mortgage in Canada. By the end, you should better understand the process and related terms to help you find the best mortgage rate in Canada.

A mortgage is a loan used to purchase a property. The property serves as collateral for the loan. In Canada, mortgages are typically amortized over 25-30 years, but the term (the length of your agreement with a specific lender) is usually shorter, often 5 years. Learn more about mortgage basics here.

A mortgage rate is the interest rate you pay on your mortgage. It's expressed as a percentage and can be fixed (staying the same for the term of your mortgage) or variable (fluctuating with the prime rate). The rate you receive depends on various factors, including your credit score, down payment, and the type of property you're buying. Explore our guide on understanding mortgage rates for more information.

Current mortgage rates vary depending on the type of mortgage (fixed or variable) and the term length. As of February 2025, 5-year fixed rates are ranging from 4.5% to 5.5%, while variable rates are typically 0.5% to 1% lower. However, rates can change daily, so it's best to check with Canada Home Ownership for the most current rates.

At Canada Home Ownership, we update our advertised rates daily to ensure you always have access to the most current information. However, the actual rate you receive may differ based on your personal financial situation and the specific details of your mortgage application. Contact one of our advisors for a personalized rate quote.

Canadian mortgage rates can change frequently, sometimes even daily. Fixed rates are influenced by bond yields, which can fluctuate based on economic conditions. Variable rates are tied to the Bank of Canada's overnight rate, which is typically reviewed eight times per year. Stay informed about rate changes by subscribing to our mortgage rate updates newsletter.

Are you navigating the complex world of Canadian mortgages? Whether you’re a first-time homebuyer or looking to renew or refinance, understanding mortgage rates is crucial. Let’s dive into the most frequently asked questions our Canada Home Ownership mortgage advisors receive daily.

Searching for the best mortgage rates in Canada can be overwhelming, especially for first-time homebuyers. With numerous terms, options, and lenders to consider, where do you begin? This comprehensive FAQ guide will break down the essentials, helping you make informed decisions about your mortgage.

By the end of this guide, you’ll have a solid understanding of the Canadian mortgage landscape, empowering you to find the best mortgage rate for your unique situation.

A: Canada offers several mortgage types to suit different financial situations:

Each type has its advantages and considerations. Our Canada Home Ownership advisors can help you determine which option best fits your needs.

A: Several factors affect mortgage rates, including:

Understanding these factors can help you anticipate rate changes and make informed decisions.

A: To secure the most competitive rates:

Remember, the lowest rate isn’t always the best option. Consider the overall cost and terms of the mortgage.

Armed with this knowledge, you’re better equipped to navigate the Canadian mortgage landscape. For personalized advice and access to competitive rates, reach out to our expert advisors at Canada Home Ownership.

Stay informed about the latest mortgage trends and rates by following updates from the Bank of Canada and the Canada Mortgage and Housing Corporation (CMHC).

For additional resources, check out:

Remember, finding the right mortgage is about more than just rates – it’s about securing your financial future and making your homeownership dreams a reality.

Welcome to our Frequently-Asked Questions (FAQ) section, where we answer the most popular questions our Canada Home Ownership mortgage advisors receive daily, designed to help you make informed mortgage decisions whenever you need a new mortgage or renew/refinance an existing one.

Are you a first-time buyer?

Mortgage shopping can be confusing, especially if you're a first-time home buyer. There are a lot of different terms and options out there, and it can be tough to know where to start. This section will cover some of the most common questions and terms when shopping for a mortgage in Canada. By the end, you should better understand the process and related terms to help you find the best mortgage rate in Canada.

A mortgage is a loan used to purchase a property. The property serves as collateral for the loan. In Canada, mortgages are typically amortized over 25-30 years, but the term (the length of your agreement with a specific lender) is usually shorter, often 5 years. Learn more about mortgage basics here.

A mortgage rate is the interest rate you pay on your mortgage. It's expressed as a percentage and can be fixed (staying the same for the term of your mortgage) or variable (fluctuating with the prime rate). The rate you receive depends on various factors, including your credit score, down payment, and the type of property you're buying. Explore our guide on understanding mortgage rates for more information.

Current mortgage rates vary depending on the type of mortgage (fixed or variable) and the term length. As of February 2025, 5-year fixed rates are ranging from 4.5% to 5.5%, while variable rates are typically 0.5% to 1% lower. However, rates can change daily, so it's best to check with Canada Home Ownership for the most current rates.

At Canada Home Ownership, we update our advertised rates daily to ensure you always have access to the most current information. However, the actual rate you receive may differ based on your personal financial situation and the specific details of your mortgage application. Contact one of our advisors for a personalized rate quote.

Canadian mortgage rates can change frequently, sometimes even daily. Fixed rates are influenced by bond yields, which can fluctuate based on economic conditions. Variable rates are tied to the Bank of Canada's overnight rate, which is typically reviewed eight times per year. Stay informed about rate changes by subscribing to our mortgage rate updates newsletter.

Are you a first-time buyer?

Understanding the factors that influence your mortgage rate is crucial for making informed decisions about homeownership in Canada. This comprehensive guide will explore the key elements that lenders consider when determining your mortgage rate.

Your credit score is a crucial factor in determining your mortgage rate. A higher credit score typically results in better rates. Here's a general breakdown:

Lenders assess your income stability and employment history to ensure you can make mortgage payments. They typically require:

For self-employed individuals, additional documentation may be required:

The size of your down payment affects your loan-to-value (LTV) ratio, which influences your mortgage rate:

Understanding these factors can help you secure the best possible mortgage rate. Remember to:

For personalized advice tailored to your unique circumstances, consult with a licensed mortgage professional or financial advisor.

North America Wide. Canada Home Ownership Inc

© Copyright by Canada Home Ownership 2003-2025